The Quantum Bubble: Last Stretch? (Part 3)

We were right. The recent collapse across these quantum names was predictable, and the underlying financials dictate that the selloff is far from over.

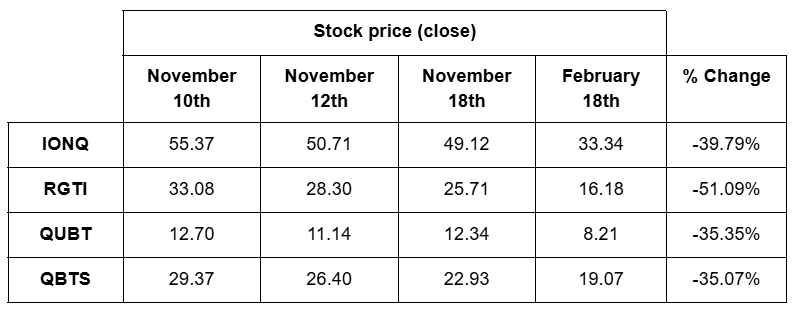

On November 10th, we mentioned we were working on a short report on quantum computing companies. On November 12th, we published Part 1, and on November 18th, Part 2 of our report, covering Quantum Computing (QUBT), D-Wave Quantum (QBTS), IonQ (IONQ), and Rigetti Computing (RGTI), exposing their fraudulent claims and exactly why they were overvalued. Since then, all four stocks have collapsed by at least 35%…

We did not, however, specify an exit strategy for this short idea. We intend to outline that now. As noted in Part 1, QUBT is effectively an empty shell kept afloat entirely by shareholder dilution. Without a miraculous operational turnaround, it has virtually no path to becoming a functional business.

While retail frenzy could resurface and temporarily squeeze some participants out of the trade, our view is that the peak risk has passed. The short thesis remains fully intact and will continue until the equity is priced near zero. Because the underlying intrinsic value is practically nonexistent, holding or tactically adding to this short position remains a sound approach.

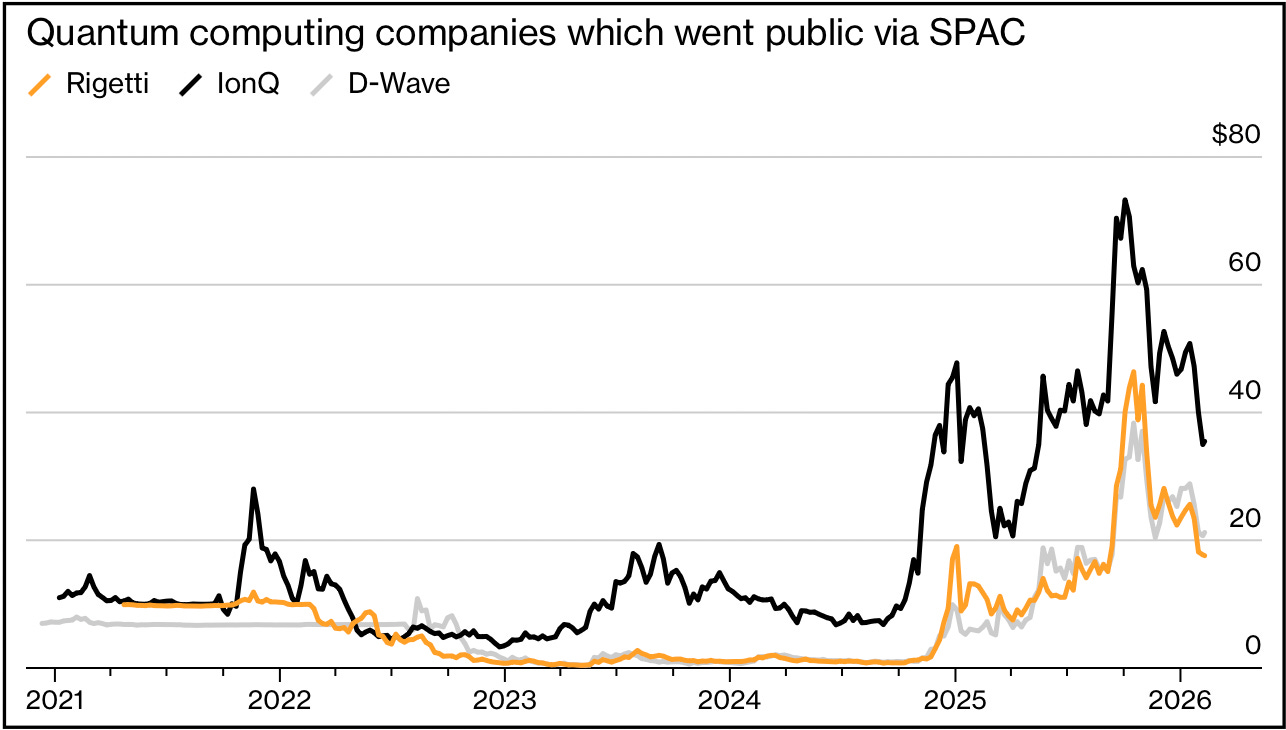

Quantum SPAC Names Fall Back Toward Penny Levels

Moving to QBTS, the situation is different. While not a complete fraud, the company uses the quantum name in a misleading way, as we believe they have no functioning quantum product. They do generate ~$8.8M in annual revenue, but this relies heavily on clients not fully understanding D-Wave's technological reality. Even if D-Wave continues to earn a few million dollars each year, the financials show a clear problem. The company lost $143.9M in 2024. With a market capitalization of $7.1B, the stock is profoundly overvalued.

The Timeline Problem

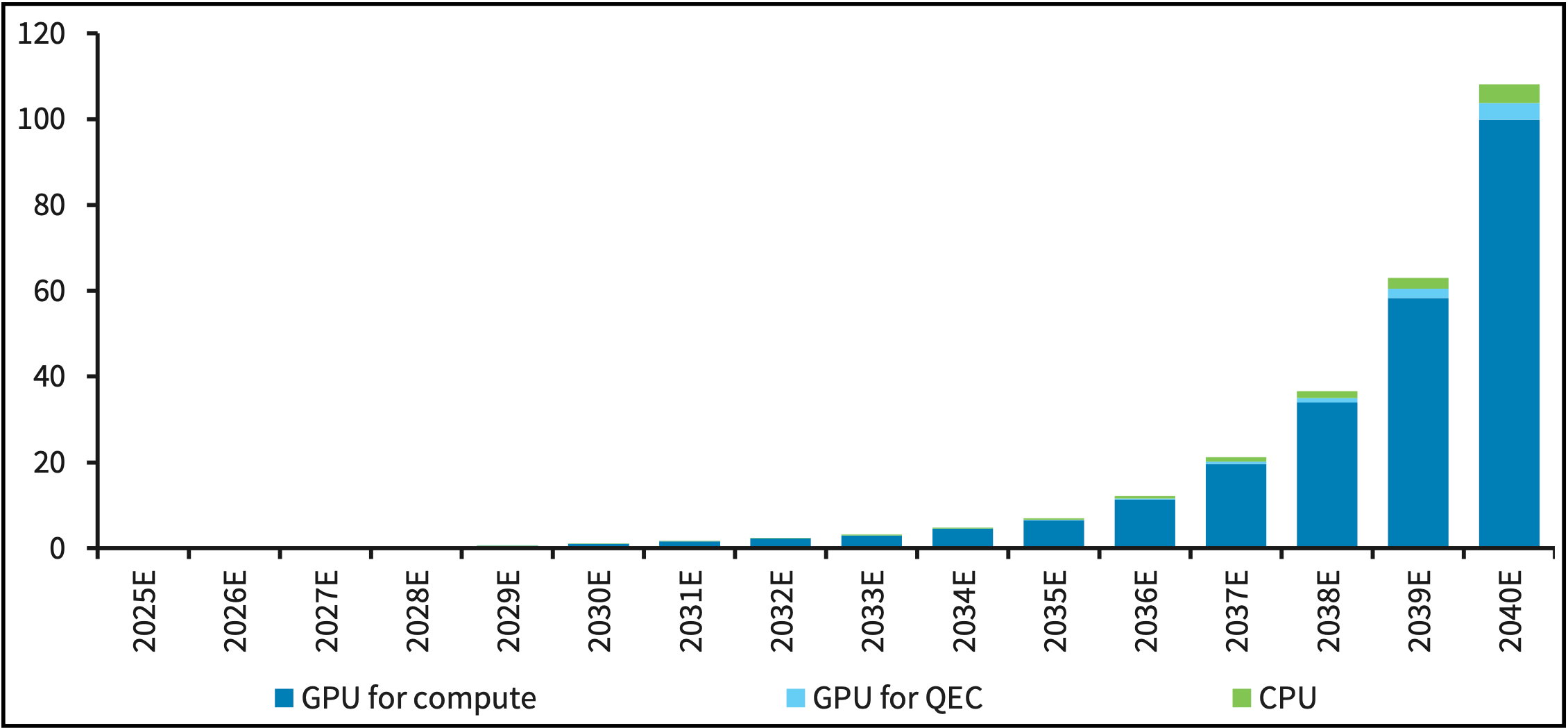

Let us look at the broader industry timeline to understand why this market exuberance is completely premature. The narrative driving these valuations relies on a massive future market, but the commercialization of quantum computing is moving much too slowly to justify current share prices.

As you can see below, optimistic estimates from Barclays Research clearly project that the classical computing market opportunity derived from quantum computing will remain practically at zero through 2029. This opportunity is only projected to begin growing slightly in 2030.

Quantum-Driven Classical Market Opportunity ($bn)

This assumes these highly speculative forecasts are completely accurate, which is far from guaranteed, as this broader adoption may never actually materialize. This timeline presents an insurmountable problem. We believe that given the rapid pace at which these entities are burning capital today, it is highly improbable they possess the financial resilience to survive another four to five years of severe losses while waiting for 2030.

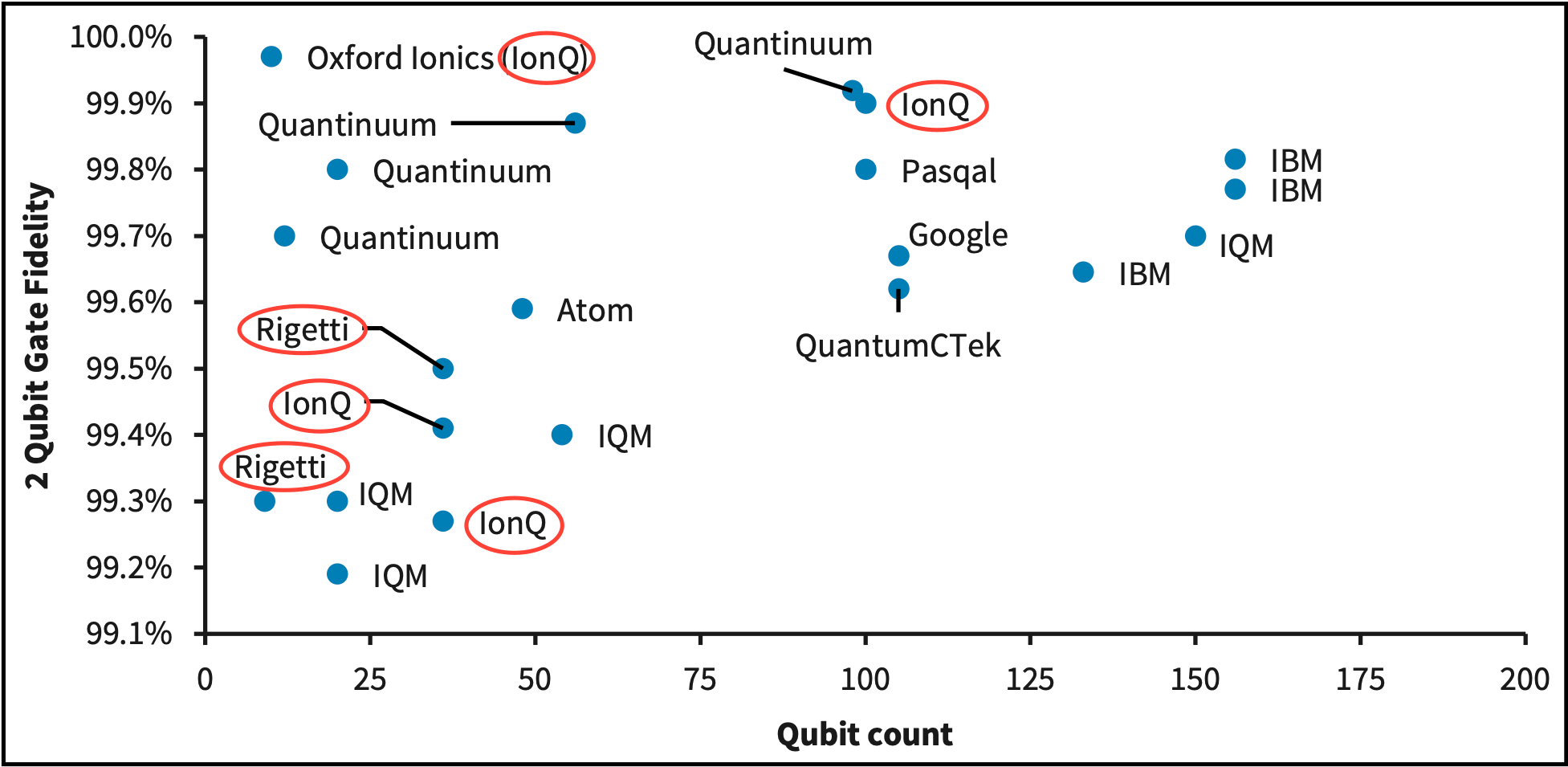

The market is pricing in a technological revolution that is simply too early and moving too fast for the underlying reality of these specific operations. Beyond the commercialization timeline, competitive positioning raises further concerns. As the benchmarking data below illustrates, IONQ and Rigetti are not leading in either qubit count or two-qubit gate fidelity when compared to larger incumbents like IBM, Google, and Quantinuum.

Barclays Quantum Benchmarking model: Qubits vs Gate Fidelity (%)

Even if industry adoption unexpectedly accelerates, we think that the structural advantages held by these deep-pocketed tech giants make it highly unlikely that smaller, cash-strapped players can bridge the gap. There is simply no clear evidence that these specific companies are positioned to emerge as dominant technological winners.

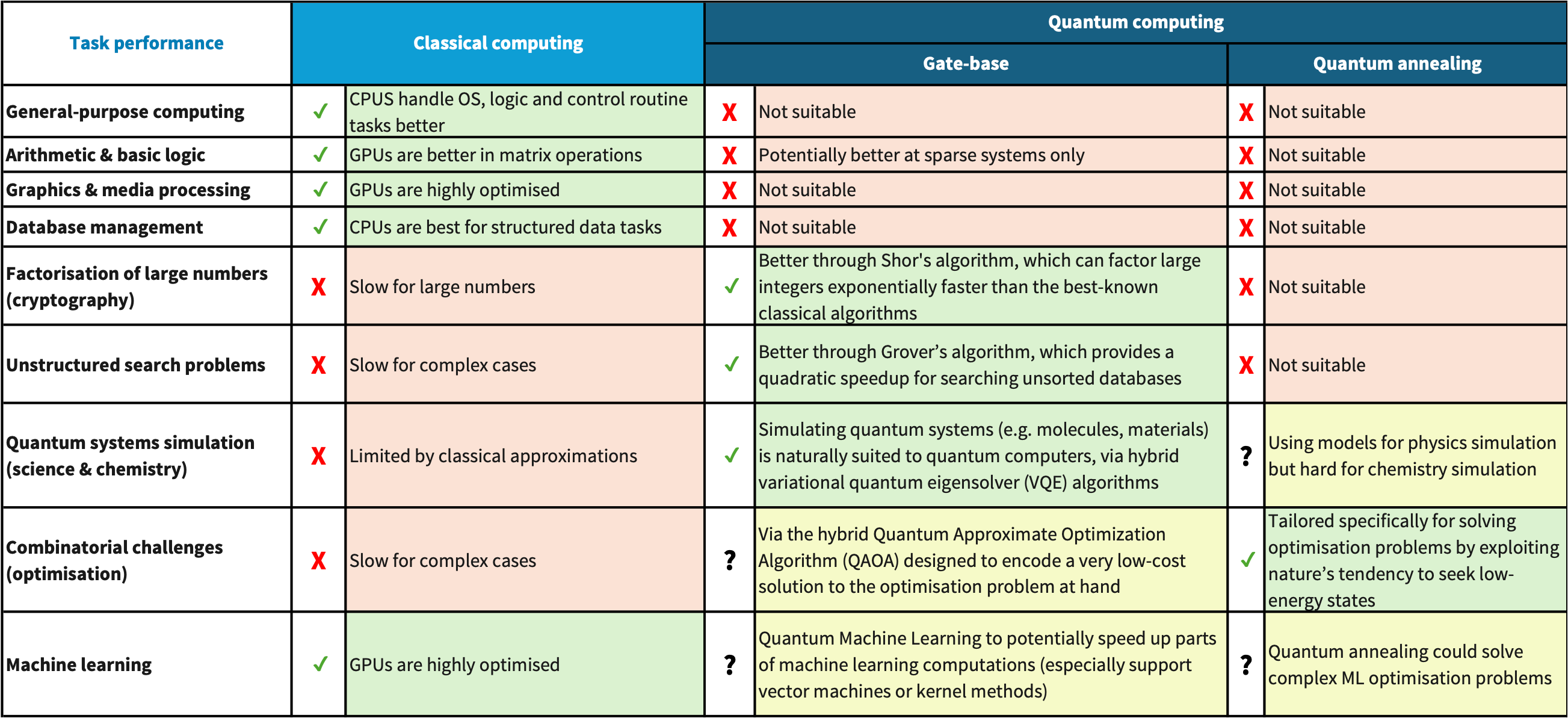

Classical Computing Still Dominates

Standard hardware remains the superior choice for almost all scientific research. The practical use for quantum systems is currently limited to a narrow range of tasks like logistics or shipping routes. While these machines can solve specific scheduling problems, they lack the flexibility required for standard data processing. Quantum technology will remain a niche application for the near term. Proven systems will continue to drive the digital economy. This bearish outlook is rooted in the reality of current hardware limitations. Most quantum systems require extreme cooling and high maintenance costs that traditional data centers do not face.

Quantum vs Classical Computing Performance Across Tasks

These machines are often fragile and prone to errors. They lack the reliability needed for the high-volume workloads modern businesses require. We see these systems as experimental technologies with limited practical use. Until error rates improve meaningfully, they are unlikely to compete with established semiconductor leaders. Proven hardware will continue to power global infrastructure, while quantum remains a costly and speculative bet.

Conversation with Quantum Expert

We spoke with practitioners in the field, including former researchers who studied quantum computing at the university level and are currently working at major firms. Having used these systems through associations with players like IBM, they share our cautious view. They are unable to see a path to commercial viability for many years and view current stock prices as driven by pure speculation, particularly as the broader equity hype begins to fade.

These experts confirm that the gap between laboratory results and commercial deployment is far wider than public markets realize. They describe current systems as promising research platforms that still lack the stability and error correction required for reliable enterprise use. In their view, many of the breakthroughs touting technical progress in press releases simply do not translate into meaningful commercial value.

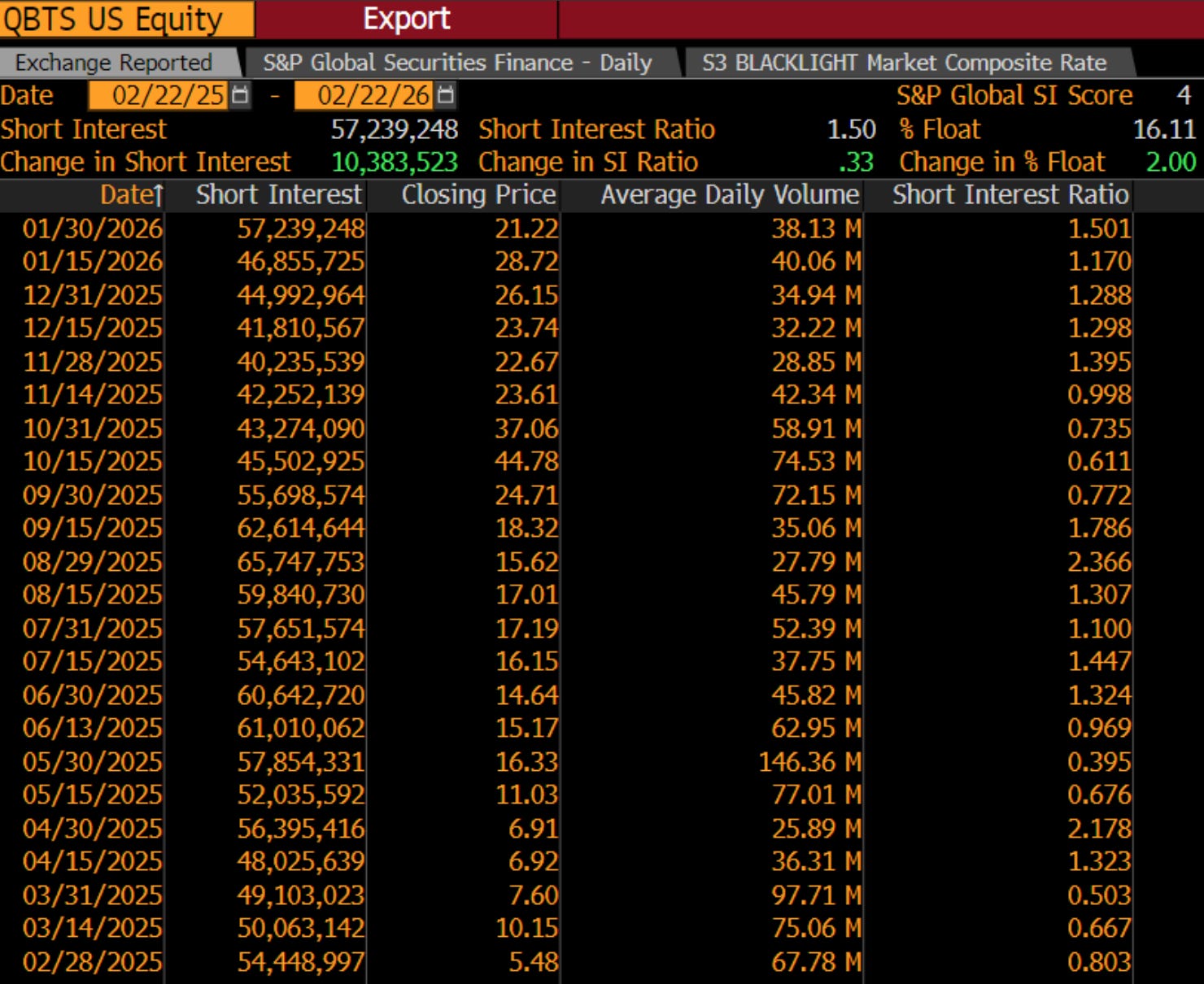

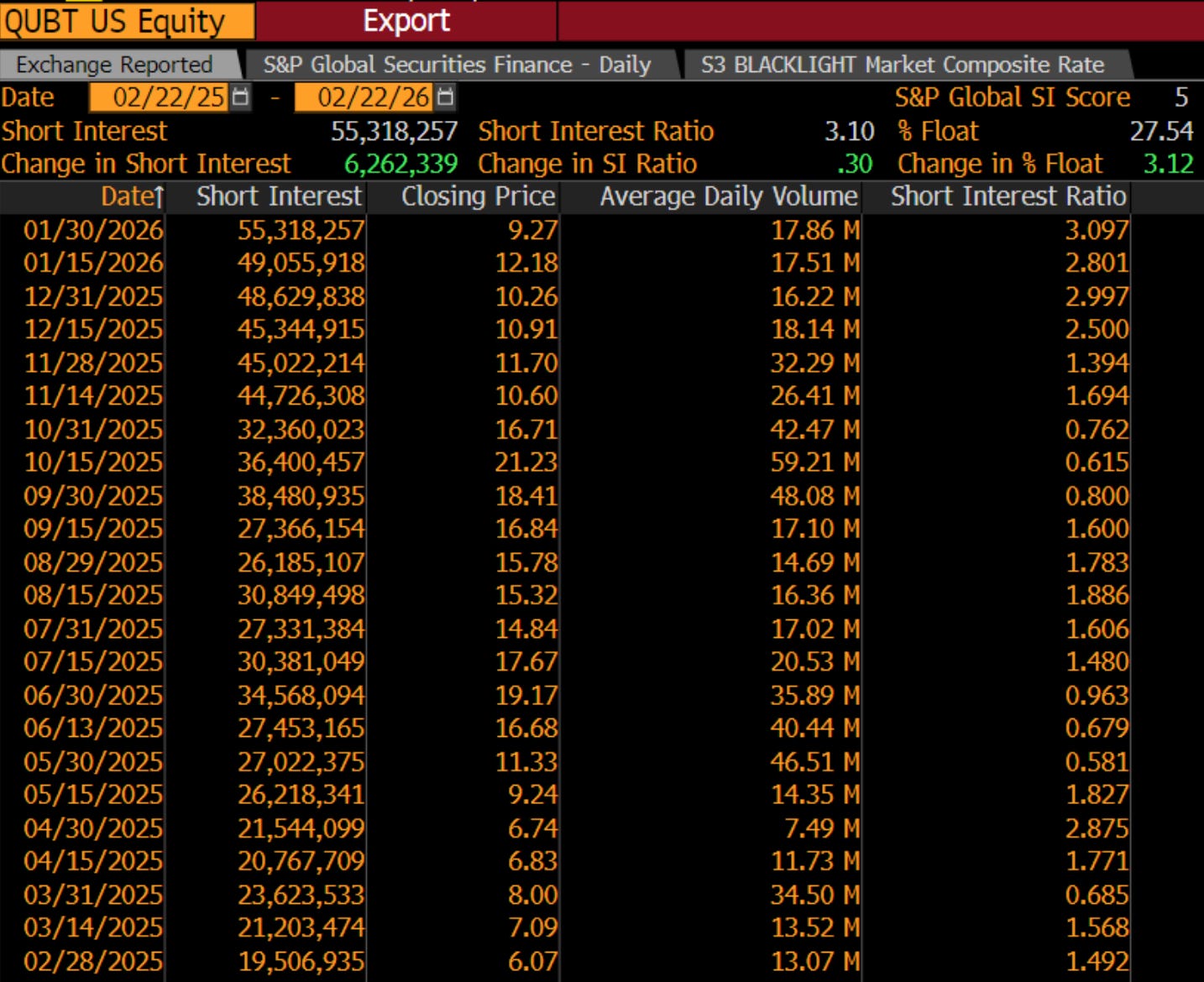

Rising Short Interest

Now, let’s examine short interest. Since we expect both stocks, QBTS and QUBT, to continue to fall drastically looking forward, it helps to look at short interest. As the data shows, for both companies, it is only rising. For QUBT, short sellers have increased their positions, pushing the total short interest to 57.2M shares. This reflects an addition of 10.3M shares in the latest reporting period. We see a similar pattern for QBTS, with its short interest reaching 55.3M shares. This now represents 27.5% of its total float. This steady increase in borrowed shares confirms our thesis, showing that the broader market recognizes the overvaluation and is positioning accordingly.

Ongoing Losses & Cash Burn

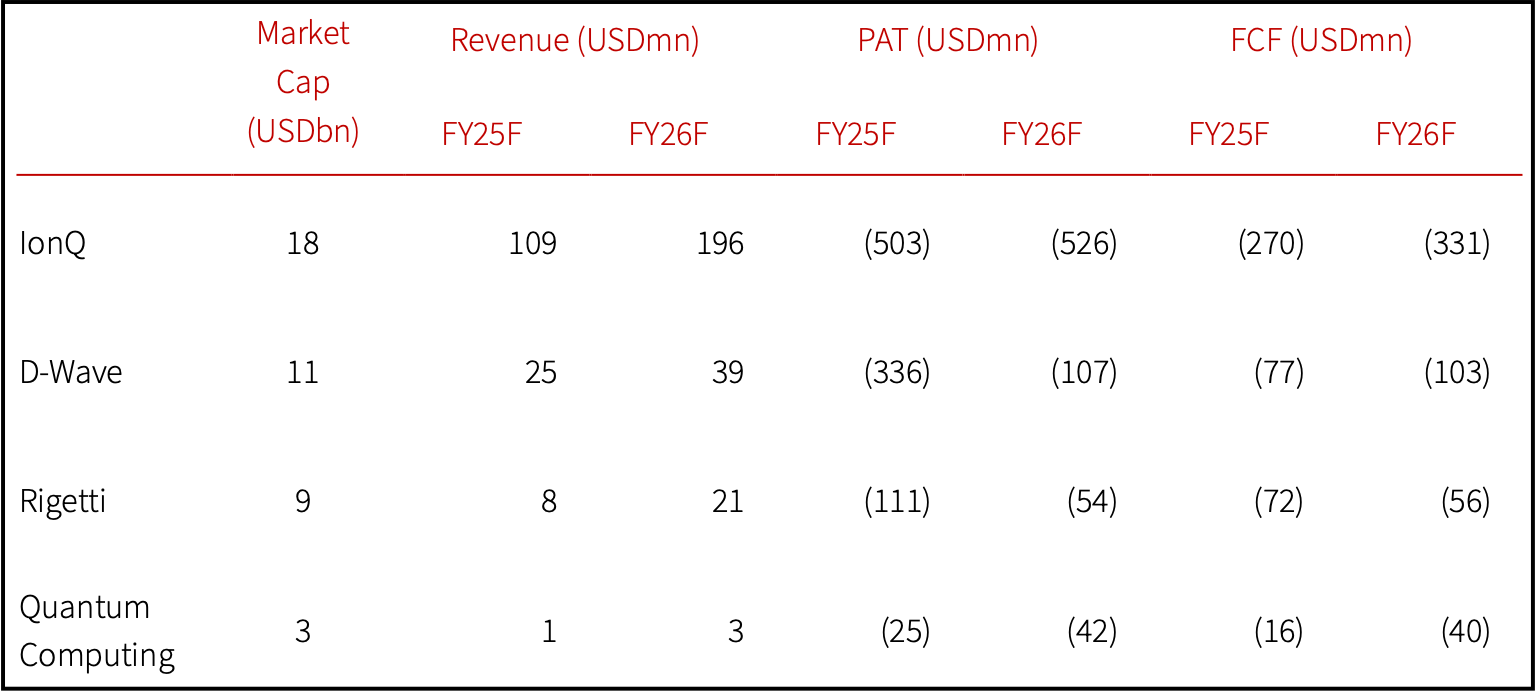

Looking ahead, and as mentioned in the previous section, the financial trajectory for these major listed quantum computing players remains exceptionally poor. Forward estimates confirm that all four entities will remain highly loss making with severe cash burn rates through at least 2026.

Projected Financial Metrics Through 2026

IonQ is projected to burn $270M in free cash flow in 2025 and $331M in 2026, alongside net losses exceeding $500M annually. D-Wave faces a similarly dire outlook, with projected free cash flows of negative $77M and negative $103M over the next two years against a mere $25M in estimated 2025 revenue.

Rigetti and Quantum Computing show the exact same fundamental flaws. QUBT is expected to generate only $1M in revenue for 2025 while recording a $25M net loss and burning $16M in cash. Across the board, these projected financials illustrate a sector entirely detached from economic reality, resting on companies guaranteed to destroy capital for the foreseeable future.

This just confirms our thinking that the current market capitalizations assigned to these entities are fundamentally irrational, and maintaining a short position across the group remains a highly logical strategy.